When I started my MBA elective of Behavioural Finance recently, my husband told me to mentally prepare to let go the Efficient Market Hypothesis (EMH). I scoffed at this. I love EMH, and it was taught to me by my favourite professor who knows everything. Back off. But as the course progressed, I could feel certain foundational beliefs start crumbling… by the end I was beaten. Long live behavioural finance.

A summary of EMH

The Efficient Market Hypothesis is basically the most influential idea about investing to have come out this side of the 1970s, and as such it probably colours your perceptions about investing even if you aren’t a finance person. The hypothesis states that stock prices reflect all available information about the company and are basically always ‘correct’ – stocks may be over- or underpriced, but only for a short while before investors recognise the mispricing and the situation corrects itself.

The beauty of the Efficient Market Hypothesis lies in how simply and elegantly it explains stock price variations. It is also a hypothesis that assumes that most people are intelligent and rational, which I would also like to believe. It’s not that there aren’t any stupid investors out there, but they are in the minority and their effect on prices will be smoothed out by the rational majority. The theory’s main implications are likewise quite egalitarian: stock-picking is very, very hard because few people have better information than everyone else, and consequently most people had better put their money into tracker funds. All good so far.

But elegance and an ideological fit are not good reasons to cling onto a theory if there is evidence to the contrary, and the behavioural finance school of thought does turn out to have a few key pieces of evidence to contradict EMH. EMH may be beautiful and satisfying on paper, but does it actually describe how people act in the real world?

The first wobble

I felt the first tremors of my shaking faith on seeing this graph of post-earnings-announcement price drift:

What is shown here is the effect of a surprising announcement concerning earnings, at date 0 on the x axis. The horizontal lines are the stock prices of companies, the top one being a company that makes an announcement that is better than investors expected and the bottom one being a company that makes a disappointing announcement. For EMH to have any practical value, you would expect investors to absorb the news and adjust their positions within a couple of days – instead, the price drifts in the general direction of the news for up to two months! (Incidentally I also find it funny how news is obviously leaking out before the announcement, as well.)

The way behavioural finance theory explains this is that investors are just people – they have other things to do than watch stock news every minute of every day. Even when they do, they might miss things and catch up a bit later. It might also well be that many investors see a stock headed one way and jump on the bandwagon just because everyone else seems to be doing it. Certainly sounds like people, doesn’t it?

The second wobble

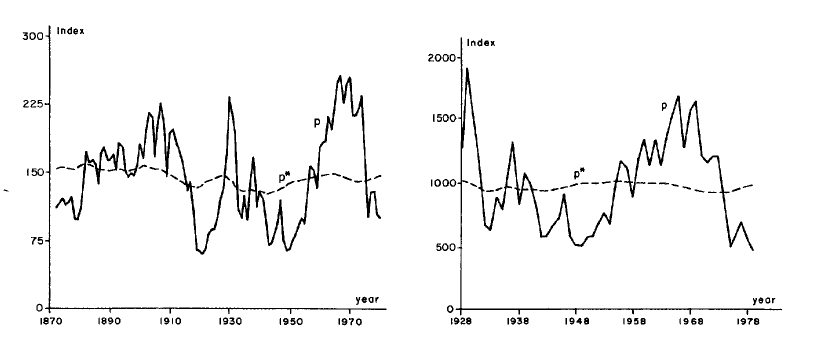

My second wobble happened when we discussed economist Robert Shiller’s work on excess volatility. He won a Nobel price for trying to back out historical stock prices from dividends actually paid out by the companies, which should be possible under EMH. He showed that they didn’t match – not even close: whatever information investors were pricing into their trades was in hindsight not accurate. These are his graphs:

For Efficient Market Hypothesis to hold, you would want to see prices predict future dividends; perhaps not in perfect lockstep but at least roughly. As you can see, that doesn’t seem to be happening at all – prices jump up and down while actual dividends are much less volatile. Of course, my EMH-loving mind suggested, it could just be that the time periods don’t match up – maybe the prices seen in 1910, for example, would be a perfect prediction of dividends in 1980 which is just outside the graph. And who knows, maybe that’s the case – but if you had to assume that stock prices reflect earnings nearly a lifetime away, that would also make EMH a pretty pointless theory.

The behavioural case here is simple: investors aren’t rational! They alternate between panicking and being boisterously optimistic, following news stories to sometimes right and sometimes wrong conclusions, taking advice from each other, their psychics, their favourite financial wonks and grandmothers, and the result is the zig-zag pattern we see above.

The death blow

The hardest thing to counter that I found on the course was the case of MCI and MCIC. MCI and MCIC are the tickers (identifiers) of the shares of two companies, Massmutual Corporate Investors and MCI Communications respectively. Incredibly, in 1996 when it was announced that BT had made a bid for MCIC, MCI’s share price went up along with MCIC’s. In a few months’ time when BT said it was renegotiating the terms of the agreement, both companies’ share prices fell. This pattern continued to happen through the period even though the companies had nothing to do with each other, making it obvious that there were considerable numbers of investors who were either too lazy or too ignorant to realise they were trading the wrong stock. If they didn’t check which stock they were buying or selling, how likely is it they read the company’s financial statements? I call this one for behavioural finance as well. By the way, it’s not the only time it’s happened!

Is all lost for EMH?

I still have a soft spot for the Efficient Market Hypothesis. I think it is at the very least a great base to build more pragmatic theories of investor behaviour on. If anyone knows of good counter-arguments to the three arguments above, I would love to be proved wrong!

Be First to Comment